KYC requirements for crypto companies are substantively the same as for other financial institutions — but come with unique challenges. Here is what crypto KYC requires, what the red flags are, and how to build a compliant program.

What Is Crypto KYC? Identity Verification for Cryptocurrency Companies

Cryptocurrency companies often operate under the misconception that KYC requirements are somehow different for them than for traditional financial institutions — that the decentralized or pseudonymous nature of blockchain creates some kind of compliance exemption.

It does not. FinCEN confirmed in 2013 that cryptocurrency businesses qualifying as money transmitters are Money Services Businesses subject to the full Bank Secrecy Act — including the same KYC requirements as traditional money services businesses. And regulators have aggressively enforced these requirements against crypto companies that failed to implement adequate identity verification programs.

This article covers what KYC actually requires for crypto companies, how crypto-specific risks affect your KYC program design, and how to build a compliant program that satisfies BSA requirements and regulators.

What Crypto KYC Requires

At its core, KYC for crypto companies is the same as KYC for any covered financial institution. The requirements come from two primary sources.

The Customer Identification Program requirement under the BSA — the obligation to collect and verify the identity of customers at onboarding. For individual customers this means name, date of birth, address, and identification number verified through documentary or non-documentary means. For business customers this extends to entity verification and beneficial ownership identification and verification.

FinCEN's CDD Rule — the obligation to understand the nature and purpose of each customer relationship, assign a risk rating, conduct ongoing monitoring, and apply Enhanced Due Diligence for higher-risk customers.

These requirements apply to cryptocurrency exchanges, cryptocurrency payment processors, custodial wallet providers, and other crypto MSBs in the same way they apply to traditional money transmitters.

How Crypto KYC Differs From Traditional KYC

While the legal requirements are the same, crypto KYC has several distinctive characteristics that affect program design.

Pseudonymous Transactions Require More Robust Onboarding Controls

Traditional financial transactions are linked to clearly identified account holders. Blockchain transactions are pseudonymous — associated with wallet addresses rather than identified individuals. This means that if your onboarding KYC is weak, you may have no way to identify the real person behind subsequent transactions on your platform.

This makes front-end KYC — thorough identity verification at onboarding — more important in crypto than in many traditional financial contexts. Weak onboarding controls cannot be compensated for by transaction-level controls in the way that might be possible with named account relationships.

Cross-Border Transactions Are Common and Elevated Risk

Cryptocurrency is borderless by design. A significant proportion of cryptocurrency transactions involve counterparties in different countries, including high-risk jurisdictions. Your KYC risk rating must account for the geographic dimension of your specific customer base.

Blockchain Analytics Augments Traditional KYC

Unlike traditional banking where transaction history is institution-specific, blockchain transaction history is publicly visible on-chain. Blockchain analytics tools — platforms that analyze on-chain transaction data to identify wallet addresses associated with illicit activity — provide KYC and AML information that has no equivalent in traditional finance.

For crypto companies, blockchain analytics is a complement to traditional KYC — providing on-chain risk intelligence that helps you understand the financial history of your customers' wallets in addition to their identity.

Privacy Coins and Mixers Require Special Treatment

Customers who primarily use privacy-enhancing technologies — privacy coins like Monero or Zcash, mixing services, or other obfuscation tools — present elevated KYC risk because these technologies are specifically designed to make blockchain transaction tracing difficult. Your KYC program should address how you handle customers who primarily transact in privacy coins or who show evidence of using mixing services.

Building a Crypto KYC Program

Step 1 — Write Your CIP for Crypto Customers

Your written Customer Identification Program must cover the specific customer types your platform serves. If you serve both individual and business customers, your CIP must address both. If your platform serves both retail and institutional customers, your CIP should address the different verification approaches appropriate for each.

For crypto companies, specific CIP considerations include what transaction threshold triggers identity verification for unverified users, how you handle customers who cannot complete automated verification, and how you approach customers from high-risk jurisdictions.

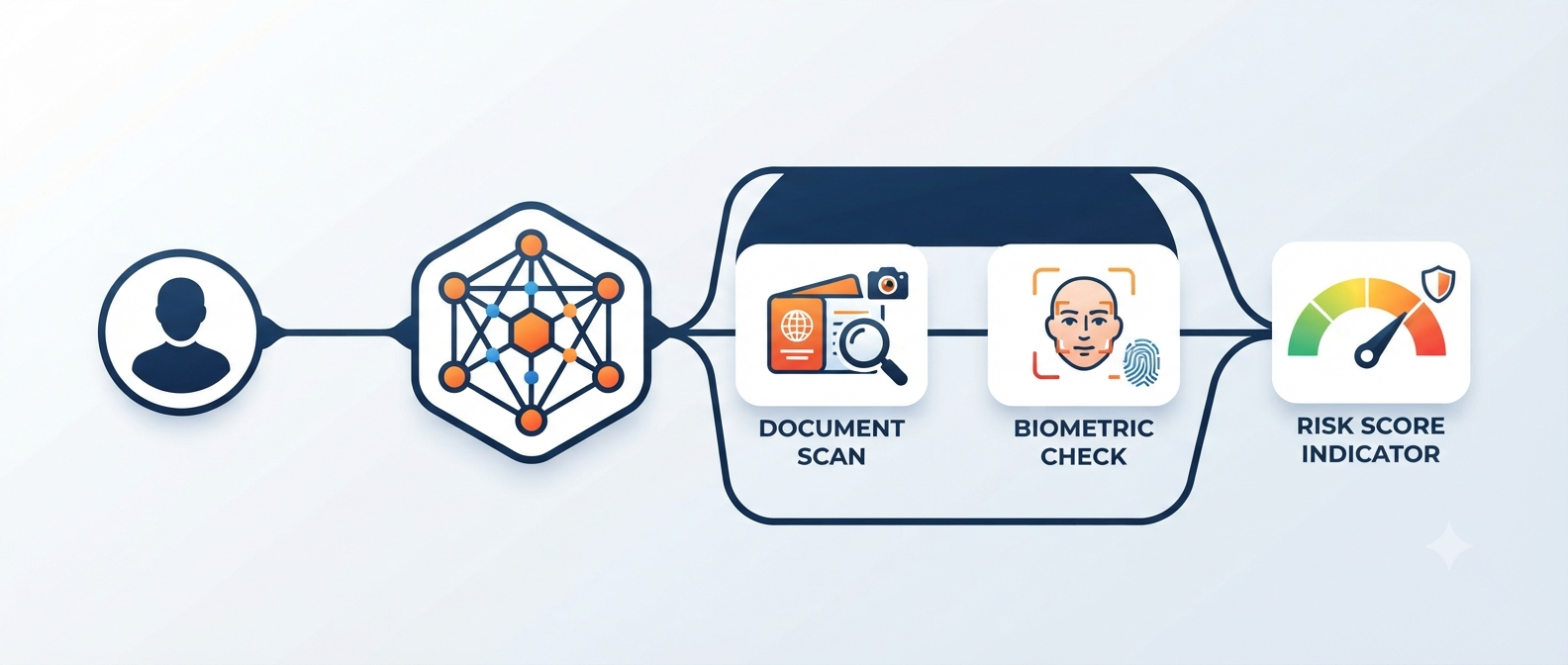

Step 2 — Select Your Identity Verification Technology

Your KYC provider must be capable of executing your CIP requirements at your onboarding volume. For crypto companies specifically, look for global document coverage to handle customers from the international jurisdictions you serve, PEP and adverse media screening at onboarding, integration with your blockchain analytics platform to enrich the onboarding risk assessment with on-chain data, and risk scoring that incorporates both identity verification results and blockchain analytics findings.

Step 3 — Integrate Blockchain Analytics Into Your KYC Risk Rating

When a customer onboards, your KYC risk rating should incorporate not just their identity information but also the risk profile of their associated wallet addresses as analyzed by your blockchain analytics platform. A customer who is a PEP is high risk. A customer who is not a PEP but whose primary wallet address shows a history of transactions with sanctioned wallets or darknet markets is also high risk — even if their identity documents are clean.

Blockchain analytics gives you a dimension of customer risk assessment that is unique to crypto and should be reflected in your risk rating methodology.

Step 4 — Apply the Travel Rule

The Travel Rule requires crypto money transmitters to collect and transmit originator and beneficiary information alongside transfers above $3,000. Implementing Travel Rule compliance requires both technology — platforms that transmit required information between regulated entities — and documented procedures for collecting and transmitting the required data.

Step 5 — Build Your EDD Procedures for Crypto-Specific Risks

Enhanced Due Diligence in the crypto context should cover PEPs as in traditional finance, customers from high-risk jurisdictions, customers whose blockchain transaction history shows elevated risk indicators identified through analytics, customers attempting to transact with privacy coins or mixing services, and high-volume traders whose activity pattern warrants closer scrutiny.

Document the specific EDD triggers for each of these categories and what EDD involves — additional documentation, additional blockchain analytics review, senior approval, enhanced ongoing monitoring. Learn more about AML red flags to watch for.

Frequently Asked Questions

Does KYC apply to DeFi platforms?

The application of KYC requirements to decentralized finance platforms is an evolving regulatory question. FinCEN's position is that the key question is whether a business or person exercises sufficient control over a protocol to be classified as a money transmitter. DeFi platforms where there is genuine decentralized control present different analysis than DeFi platforms where a developer or company maintains significant control. Any business in or building DeFi should seek qualified legal counsel on their specific KYC obligations.

What level of KYC is required for small crypto transactions?

FinCEN's regulations require identity verification for customers, but some crypto platforms apply a tiered approach — allowing small transactions with limited verification and requiring full KYC for higher transaction amounts or account types. The specific thresholds that trigger full KYC requirements depend on your business model and should be documented in your CIP. Note that structuring small transactions to avoid KYC thresholds is itself a red flag that should trigger compliance review.

How does blockchain analytics help with KYC?

Blockchain analytics platforms analyze on-chain transaction data to identify wallet addresses associated with known illicit activity — darknet markets, ransomware payments, sanctioned wallets, mixing services, and other high-risk sources. Integrating blockchain analytics into your KYC onboarding and ongoing monitoring gives you risk intelligence about your customers' transaction history that is not available through traditional identity verification alone.

How ComplyOne Helps

ComplyOne helps cryptocurrency companies build KYC programs that satisfy BSA requirements and regulatory expectations — from CIP documentation and blockchain analytics integration to EDD design and Travel Rule implementation — through advisory services, compliance technology, or both. Learn more about AML compliance for crypto.

Talk to the ComplyOne team to get started.

The information in this article is for general educational purposes and does not constitute legal or regulatory advice. Consult a qualified compliance professional for guidance specific to your situation.