Beneficial ownership rules require fintechs to identify the real humans behind business customers. Here is what the rules require, how to collect and verify beneficial ownership information, and what changed under the Corporate Transparency Act.

What Is Beneficial Ownership? Rules and Requirements for Fintechs

Beneficial ownership is one of the most important and most frequently misapplied concepts in fintech compliance. The rules around it exist for a specific reason — legal entities can be used to hide the real people behind financial transactions, making it possible to launder money, evade sanctions, or commit fraud without the actual individuals being visible. Beneficial ownership rules are designed to pierce that veil.

For fintechs that onboard business customers, understanding and correctly applying beneficial ownership requirements is not optional. FinCEN's CDD Rule makes it a formal requirement, and the Corporate Transparency Act has added a parallel federal reporting obligation that affects most U.S. companies.

What Is Beneficial Ownership?

Beneficial ownership refers to the individuals who ultimately own or control a legal entity — the natural persons behind the corporate structure. A beneficial owner is not necessarily the same as the registered owner or director of a company. In many structures, the true economic owner is one or more steps removed from the legal entity your fintech is onboarding as a customer.

FinCEN's CDD Rule defines beneficial owners as individuals who meet either of two tests.

The Ownership Prong

Any individual who directly or indirectly owns 25 percent or more of the equity interests of the legal entity. This includes direct equity holders and individuals who own equity indirectly through intermediate entities.

If no individual owns 25 percent or more — for example a company with six equal shareholders each owning approximately 17 percent — the ownership prong results in no beneficial owners identified under that test. This is a documented outcome, not an error.

The Control Prong

One individual who exercises significant management control over the entity regardless of their ownership percentage. This is typically the CEO, President, Managing Member, General Partner, or equivalent executive — the person who makes significant decisions for the entity on a day-to-day basis.

Every legal entity customer has at least one beneficial owner identified under the control prong — even if no individual meets the 25 percent ownership threshold.

Why These Rules Exist

Before beneficial ownership requirements were formalized, legal entities could be structured to effectively hide their true owners. A shell company with nominee directors, owned by another shell company in an offshore jurisdiction, owned by a trust — the chain could be extended to make it practically impossible to determine who actually controlled the money flowing through the entity.

Beneficial ownership rules require financial institutions to look through these structures to identify the real humans who own and control their business customers. This makes it significantly harder to use corporate entities as money laundering vehicles, sanctions evasion tools, or fraud instruments.

What Fintechs Must Do Under FinCEN's CDD Rule

FinCEN's CDD Rule requires covered financial institutions — which includes most MSBs and fintechs operating under sponsor bank arrangements — to collect and verify beneficial ownership information for legal entity customers at onboarding.

Collection

At onboarding, collect beneficial ownership information for every business customer. This means identifying all individuals meeting the ownership prong, the one individual meeting the control prong, and collecting the following for each: full legal name, date of birth, residential address, and a unique identifying number from an acceptable identification document such as a passport or driver's license along with an image of that document.

Many institutions use a beneficial ownership certification form — a standardized form completed by the customer certifying the accuracy of the beneficial ownership information provided.

Verification

Collecting the information is not sufficient. FinCEN requires verification — confirming through documentary or non-documentary means that the individuals identified as beneficial owners are who they say they are. The most common failure in KYB programs is collecting beneficial ownership certifications from customers without conducting any independent verification of the information provided. Collection without verification is not compliant.

Verification methods include reviewing copies of government-issued ID documents for each beneficial owner, cross-referencing the provided information against identity verification databases, and where complex ownership structures are involved, reviewing corporate formation documents to verify the ownership chain.

Ongoing Monitoring and Updating

Beneficial ownership information is not static. Business customers change ownership — through investment rounds, equity transfers, acquisitions, and ownership restructuring. Your program must have a process for identifying and capturing material changes to beneficial ownership during the customer relationship.

Periodic KYB reviews — at intervals defined by customer risk rating — should include verification that beneficial ownership information remains current.

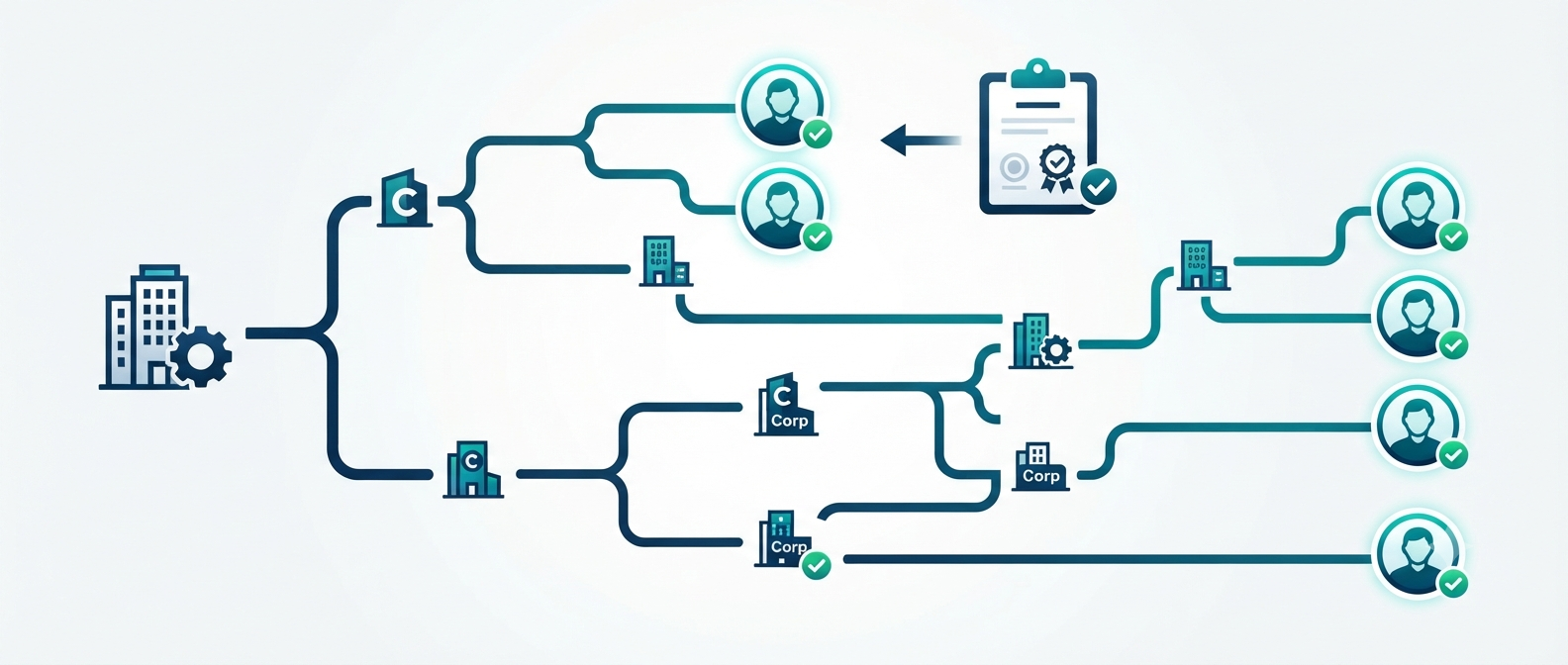

Tracing Ownership Through Multiple Layers

When a business customer is owned by another legal entity rather than directly by individuals, you must trace the ownership chain through each layer until you reach the ultimate natural person beneficial owners.

For example: Your fintech customer is ABC LLC, which is 100 percent owned by XYZ Holdings Inc., which is 80 percent owned by Individual A and 20 percent owned by Individual B. In this case Individual A and Individual B are the beneficial owners under the ownership prong — even though neither is a direct owner of ABC LLC.

Your CDD policy must define how many ownership layers you trace, how you handle structures where tracing is not possible, and how you document the outcome when full tracing to natural persons cannot be completed.

The Corporate Transparency Act — A Parallel Obligation

The Corporate Transparency Act, effective January 1, 2024, created a parallel beneficial ownership reporting obligation for most U.S. companies. Under the CTA, most small and mid-sized U.S. companies are required to file beneficial ownership information directly with FinCEN's Beneficial Ownership Information database.

This obligation runs in the opposite direction from the CDD Rule. Under the CDD Rule, financial institutions must collect beneficial ownership from their customers. Under the CTA, companies must proactively report their own beneficial ownership to FinCEN.

These are separate, parallel obligations. The CTA does not eliminate financial institutions' independent obligation to collect and verify beneficial ownership from their business customers. The FinCEN BOI database is not currently publicly accessible — financial institutions cannot rely on CTA filings to satisfy their CDD Rule verification requirements.

Frequently Asked Questions

What if a customer refuses to provide beneficial ownership information?

If a business customer refuses to provide required beneficial ownership information, the relationship cannot proceed. Onboarding a business customer without collecting and verifying required beneficial ownership information is a BSA compliance failure. If a customer refuses, document the refusal and do not open the account.

Does beneficial ownership apply to all business customers?

FinCEN's CDD Rule applies to legal entity customers — corporations, LLCs, limited partnerships, and other entities formed by filing with a state authority. Sole proprietors operating under their own name are generally treated as individual customers rather than legal entity customers for CDD purposes, though this depends on the specific facts.

What is the difference between the 25 percent threshold and the control prong?

The 25 percent threshold identifies beneficial owners based on economic ownership — who owns enough of the entity to have a material economic interest. The control prong identifies beneficial owners based on management control regardless of ownership percentage — ensuring that someone who controls an entity through management authority rather than equity ownership is still identified.

How ComplyOne Helps

ComplyOne helps fintechs build beneficial ownership collection and verification programs that satisfy FinCEN's CDD Rule requirements, handle complex ownership structures correctly, and integrate with their broader KYB onboarding operations — through advisory services, compliance technology, or both.

Talk to the ComplyOne team to get started.

The information in this article is for general educational purposes and does not constitute legal or regulatory advice. Consult a qualified compliance professional for guidance specific to your situation.