A compliant KYC program covers identity verification, risk rating, ongoing monitoring, and EDD. Here is how to build one from scratch — step by step — that satisfies BSA requirements and sponsor banks.

How to Build a KYC Program for Your Fintech

Most fintech founders understand that KYC is required. Far fewer understand exactly what a compliant KYC program must include, how to build it correctly from the start, and what regulators and sponsor banks actually look for when they review it.

This guide covers all of it. What a KYC program must include, how to build each component, what technology you need, and how to know when your program is ready for a sponsor bank review.

What a KYC Program Must Include

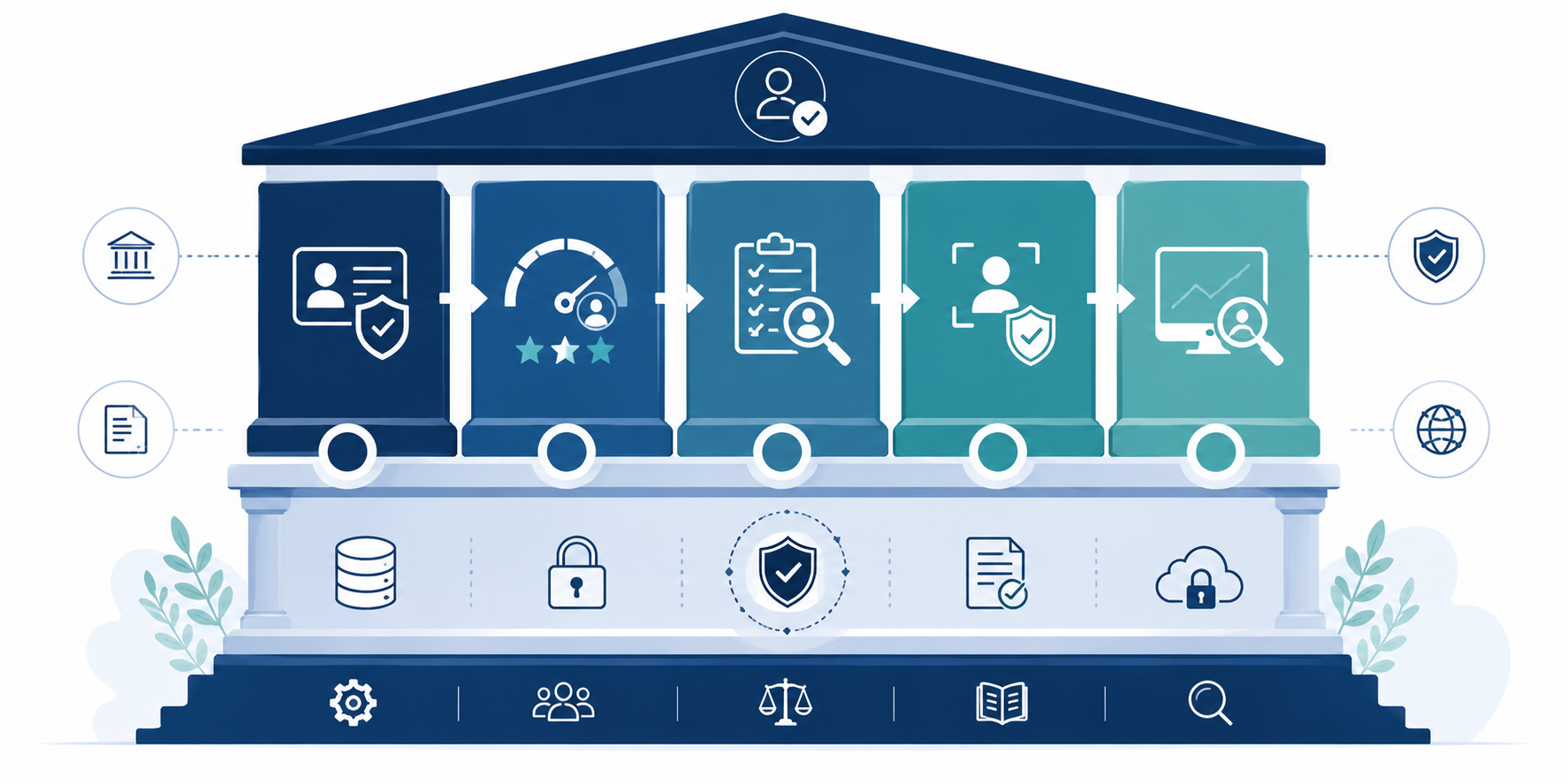

A compliant fintech KYC program has five required components under the Bank Secrecy Act and FinCEN's CDD Rule.

A written Customer Identification Program covering how you verify the identity of every customer at onboarding. Customer risk rating procedures defining how you assess the risk each customer represents. Customer Due Diligence procedures covering ongoing monitoring and periodic review. Enhanced Due Diligence procedures for higher-risk customers including PEPs, high-risk geographies, and complex business structures. And a documented process for updating customer information when risk profiles change.

Each of these must be documented in writing, approved by senior management, and consistently executed across your entire customer base.

Step 1 — Write Your Customer Identification Program

The CIP is the legal foundation of your KYC program. It must specify exactly what information you collect from each customer type and exactly how you verify that information.

For Individual Customers

Collect full legal name, date of birth, residential address, and identification number — for U.S. persons this is typically a Social Security Number or ITIN, for foreign nationals a passport number or equivalent government-issued document number.

Verify the information through documentary verification — reviewing a government-issued ID document — or non-documentary verification — cross-referencing the information against authoritative databases such as credit bureau records. Most fintechs use both methods through an automated identity verification provider.

Document the verification method used, the result, and the date for every customer.

For Business Customers

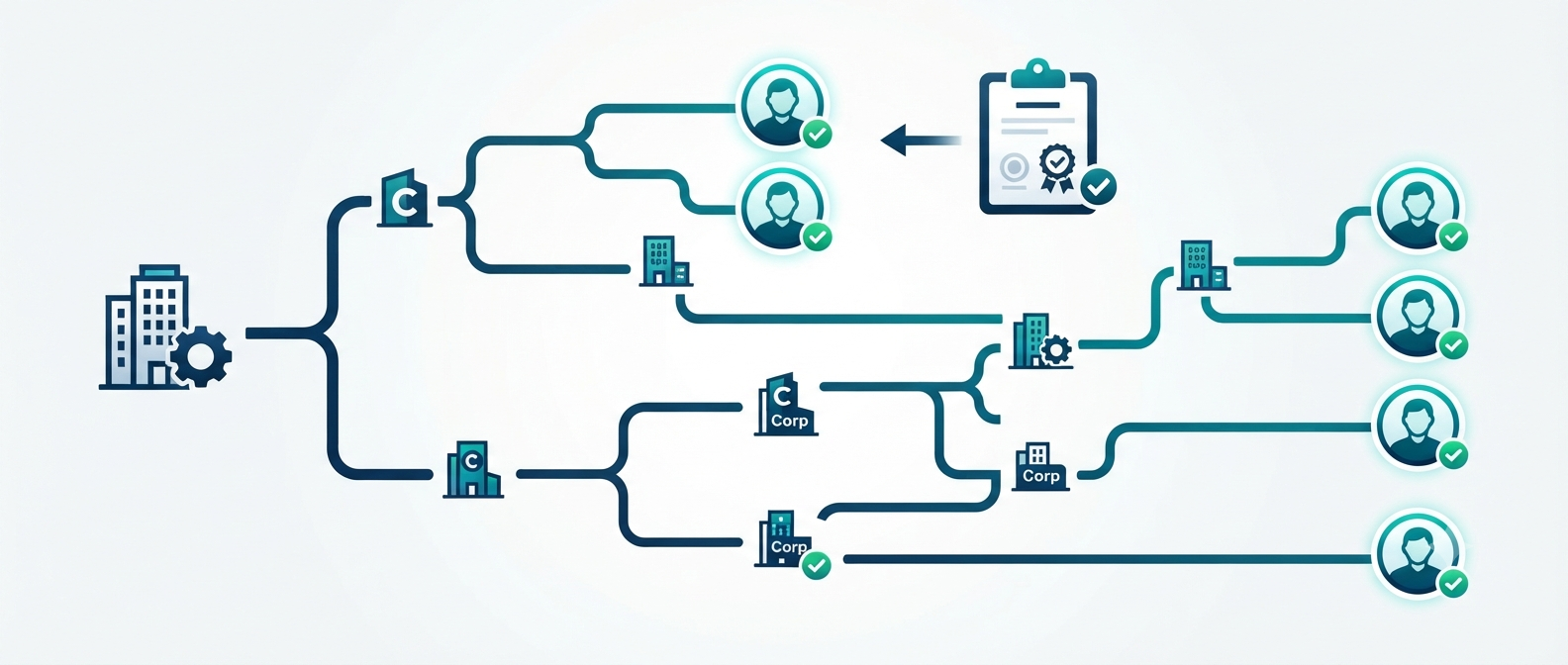

Collect legal business name, principal place of business address, Employer Identification Number, formation documents, and beneficial ownership information for all individuals who own 25 percent or more of the entity and one individual with significant management control.

Verify the entity's legal existence through formation documents and state business registry cross-reference. Verify each beneficial owner's identity using the same standards as individual customer verification.

Handling Verification Failures

Your CIP must specify what happens when verification cannot be completed — whether you restrict the account, close it, or require additional documentation before allowing transactions. Document this process and apply it consistently.

Step 2 — Build Your Customer Risk Rating Methodology

Every customer must be assigned a risk rating — typically low, medium, or high — based on objective criteria defined in your CDD policy. The risk rating determines the level of ongoing monitoring and review applied to the account.

Define the specific criteria for each tier. Low-risk criteria typically include U.S. residents, standard consumer use cases, straightforward employment or income sources, and no adverse screening results. Medium-risk criteria include non-U.S. residents, business customers in standard industries, or individual characteristics that warrant closer attention without reaching EDD thresholds. High-risk criteria include PEPs, customers from high-risk geographies, customers in high-risk industries, customers with complex ownership structures, or customers flagged by adverse media screening.

Apply risk ratings consistently using these defined criteria. Inconsistent application — where similarly situated customers receive different ratings based on individual analyst judgment — is one of the most common examination findings in KYC program reviews.

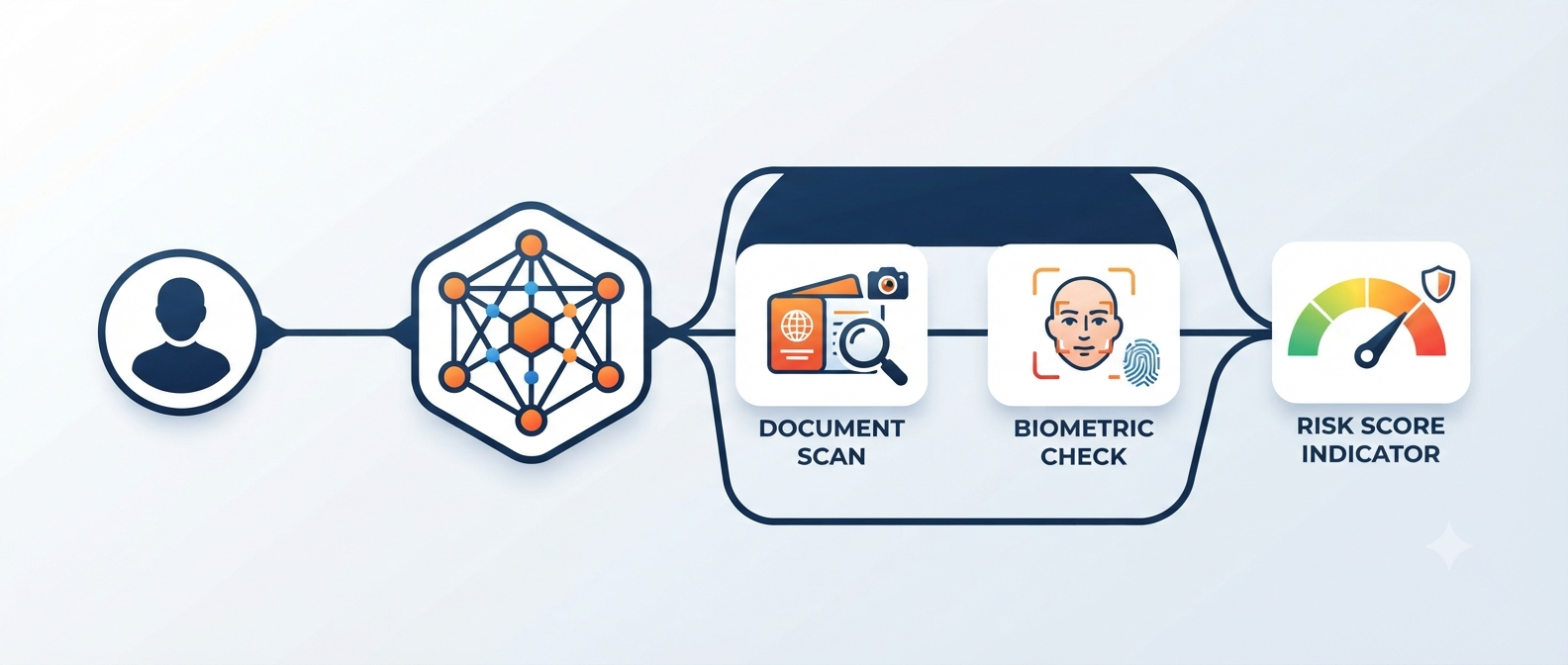

Step 3 — Implement Your Verification Technology

Your KYC compliance program cannot run manually at any meaningful customer volume. You need automated identity verification technology that executes your CIP requirements at onboarding.

Key capabilities to look for include document verification scanning and authenticity checking government-issued IDs, biometric verification confirming the person presenting the ID is the same person in the document photo, database verification cross-referencing identity information against authoritative records, PEP and sanctions screening integrated into the onboarding flow, and risk scoring that produces a documented risk assessment for each customer.

Your verification technology should produce a complete, timestamped audit trail for every onboarding — showing what information was collected, what verification steps were taken, what the results were, and when each step occurred. This audit trail is what you produce in an examination.

Step 4 — Build Your Ongoing Monitoring Process

KYC is not a one-time onboarding exercise. Your program must include ongoing monitoring of customer activity against the expected profile established at onboarding.

Your transaction monitoring system executes this in practice — detecting activity that deviates from the customer's expected behavior and generating alerts for compliance review. The CDD requirement is that your compliance program is capable of connecting monitoring alerts to customer-level risk reassessment when appropriate.

Define the circumstances under which a monitoring alert triggers a CDD review — reassessment of the customer's risk rating, request for updated customer information, or escalation to EDD if new risk factors emerge.

Step 5 — Build Your EDD Procedures

For customers who meet your defined EDD criteria, your program must specify what Enhanced Due Diligence involves — what additional documentation is collected, what approval is required before onboarding proceeds, what more intensive monitoring parameters apply, and how frequently periodic reviews occur.

Common EDD triggers include PEP status, residence or operation in a FATF grey or black list country, operation in a high-risk industry such as cannabis or cryptocurrency, and complex or opaque business ownership structures.

Document every EDD decision — the trigger, the additional information collected, the approval obtained, and the conclusion reached.

Step 6 — Establish Your Periodic Review Schedule

Your CDD program must include periodic reviews of customer information at intervals defined by risk rating. High-risk customers should be reviewed at least annually. Medium-risk customers every 18 to 24 months. Low-risk customers every three to five years or when triggered by monitoring activity.

Periodic reviews should reassess the customer's risk rating, verify that identity information remains current, and confirm that expected account activity still aligns with observed behavior.

Step 7 — Write and Approve Your KYC Policy

Document everything above in a written KYC policy that is approved by senior management. The policy should describe your CIP requirements, your risk rating methodology, your verification technology and process, your ongoing monitoring integration, your EDD triggers and procedures, and your periodic review schedule.

The policy must be specific to your business — not a generic template — and must accurately reflect how your program actually operates.

What Regulators and Sponsor Banks Evaluate

When examiners or sponsor banks review your KYC program they evaluate whether the CIP is written, complete, and consistently executed, whether verification is actually occurring — not just information collection, whether risk ratings are applied consistently using documented criteria, whether ongoing monitoring connects to CDD when risk profiles change, whether EDD is applied to all customers meeting defined triggers, and whether the documentation in individual customer files matches what the policy says should happen.

Consistency of execution across your entire customer base is as important as the design of the program itself.

Frequently Asked Questions

How long does it take to build a KYC program?

Building a KYC program involves writing the policy, selecting and implementing identity verification technology, configuring your risk rating criteria, and training your team. For an early-stage fintech starting from scratch, a basic functional KYC program can be built in four to eight weeks with focused effort. More complex programs for businesses serving diverse customer types or high-risk segments take longer.

Can I use a third-party KYC provider and still own my KYC program?

Yes. Using a third-party KYC provider to execute the verification steps of your CIP does not mean the provider owns your KYC program. Your business remains responsible for having a written CIP, applying it consistently, and maintaining the documentation that demonstrates compliance. The provider is a tool your program uses — not a replacement for the program itself.

What is the most common reason KYC programs fail in examinations?

Inconsistency between the written program and actual execution is the most common finding. Programs that describe a rigorous verification process but have customer files showing incomplete verification, or that define a consistent risk rating methodology but have customers with similar profiles rated differently, fail examinations not because the program design is wrong but because it is not being consistently applied.

How ComplyOne Helps

ComplyOne helps fintechs design and implement KYC programs that satisfy BSA requirements and sponsor bank expectations — from CIP documentation and risk rating framework design to identity verification technology selection and ongoing monitoring integration — through advisory services, compliance technology, or both.

Talk to the ComplyOne team to get started.

The information in this article is for general educational purposes and does not constitute legal or regulatory advice. Consult a qualified compliance professional for guidance specific to your situation.