Money transmitter license requirements vary dramatically by state. Here is a practical checklist of what most states require — application materials, financial documents, compliance documentation, and ongoing obligations.

Money Transmitter License Requirements: A Complete State Checklist

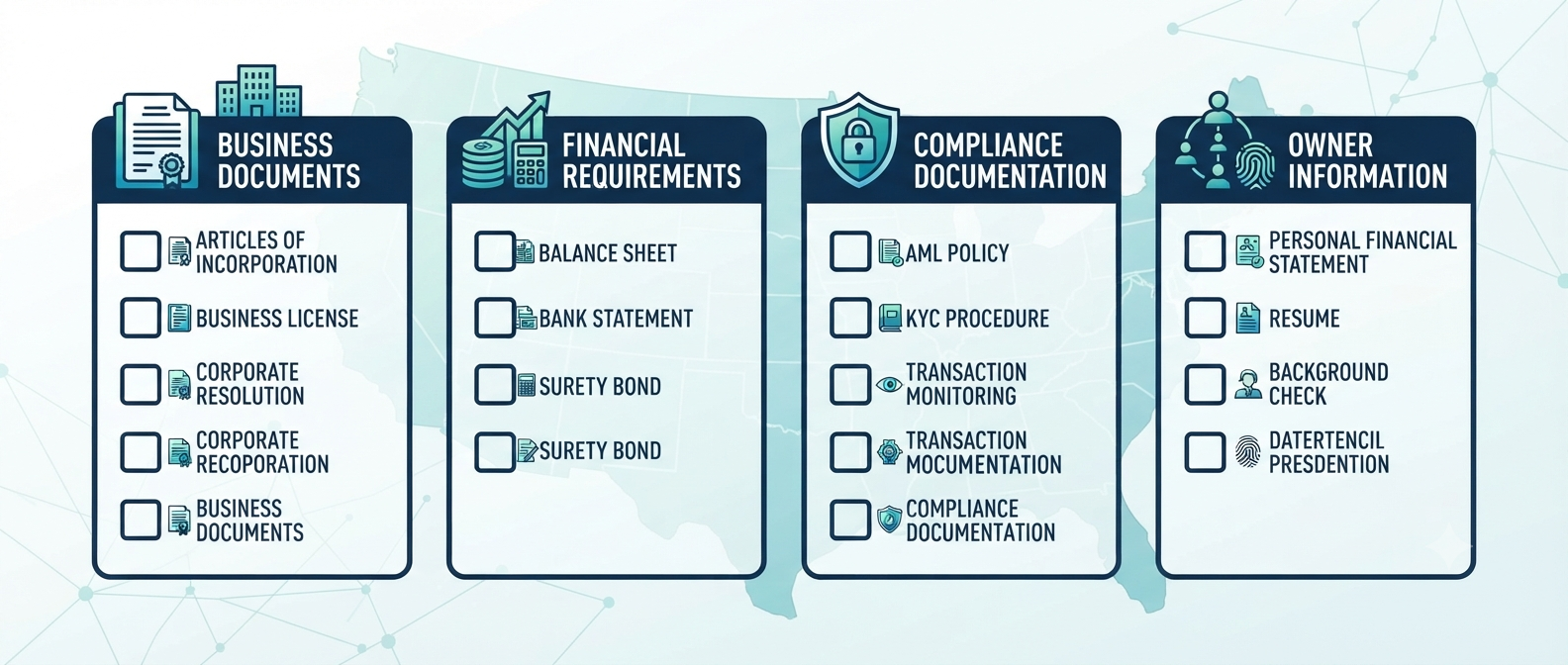

If you have decided to pursue a money transmitter license, the next question is: what do you actually need to submit? State licensing applications are comprehensive — they require significant documentation across multiple categories, and incomplete applications are one of the most common causes of delay.

This checklist covers what most states require for a money transmitter license application. Requirements vary by state — some require additional documentation, some allow alternative forms, and some have unique requirements not covered here. Always verify the specific requirements of each state you are applying in before submitting.

Business Information and Formation Documents

Every money transmitter license application begins with foundational information about your business.

Legal business name — the exact legal name under which your business is organized, as it appears in your formation documents. All trade names and DBA names your business operates under must also be disclosed.

State and date of formation — when and where your business was legally organized. For businesses formed in one state but applying to operate in another, you may need to register as a foreign entity in the application state before your license application can proceed.

Federal Employer Identification Number from the IRS — required in every state.

Formation documents — for corporations, articles of incorporation and bylaws. For LLCs, articles of organization and operating agreement. For partnerships, partnership agreement.

Certificate of good standing from your state of formation — issued by the Secretary of State or equivalent authority, typically dated within 90 days of application submission.

Foreign qualification documents if your business is organized in a different state than where you are applying — demonstrating that your business is authorized to conduct business in the application state.

Organizational chart showing your business's corporate structure — including any parent entities, subsidiaries, and affiliated companies.

Principal and Owner Information

States require detailed information about the individuals who own and control your business.

Personal information for all owners — typically all individuals owning 10 percent or more of the business, though some states use different thresholds. Required information typically includes full legal name, residential address, date of birth, Social Security Number, and contact information.

Personal financial statements for principal owners — typically for owners above a specified ownership threshold, covering assets, liabilities, and net worth.

Background disclosure — most states require disclosure of prior criminal history, prior regulatory history, prior license applications in any state, prior business failures, and any civil litigation history. Principals must disclose accurately — non-disclosure of material history is typically treated more severely than the underlying history itself.

Fingerprints for background investigation — most states require fingerprinting for all principal owners and controlling persons. The fingerprint process and submission method vary by state, with most NMLS states accepting electronic fingerprint submissions.

Government-issued photo identification — copies of valid government-issued ID for each principal.

Resumes — some states require professional resumes for principal owners and key executives demonstrating relevant financial services experience.

Financial Documentation

Financial requirements are often the most demanding category of the money transmitter license application.

Audited financial statements — most states require audited financial statements for the applicant entity for the most recent fiscal year. Some states accept reviewed financial statements for smaller businesses. Audited financials must be prepared by a licensed CPA and include the auditor's report.

If your business is newly formed and does not yet have audited financials — which is common for pre-launch fintechs — many states accept a combination of reviewed financial statements or compiled financials plus a personal financial statement for principal owners demonstrating the financial backing of the business.

Net worth documentation — demonstrating that your business meets the minimum net worth requirement for the applicable state. Net worth is calculated from your balance sheet as assets minus liabilities. States verify this against your audited financial statements.

Surety bond — a surety bond in the required amount for the state, issued by a surety company licensed to operate in the application state. Bond requirements vary by state and in many states scale with projected or actual transaction volume. The bond must name the state as obligee and meet any specific language requirements in the state's licensing statute.

Permissible investments documentation — some states require proof that the licensee holds permissible investments in an amount equal to or exceeding outstanding customer fund balances. Documentation requirements vary.

Bank account information — evidence that your business maintains a dedicated business banking relationship.

Compliance Program Documentation

States increasingly require comprehensive compliance documentation as part of the license application — not just as an afterthought.

Written BSA/AML program — your complete written AML compliance program covering internal controls, a designated compliance officer, ongoing training, independent testing, and customer due diligence. The program must be specific to your business model — generic templates are often flagged.

AML risk assessment — your completed and documented assessment of the money laundering risks your business faces based on your products, customers, geographies, and delivery channels.

Customer Identification Program — written procedures for verifying customer identity at onboarding for both individual and business customers.

KYC and CDD procedures — documented procedures for customer due diligence, risk rating, ongoing monitoring, and enhanced due diligence for higher-risk customers.

OFAC sanctions screening policy — documentation of your approach to screening customers and transactions against sanctions lists.

Compliance officer information — the name, contact information, and qualifications of your designated BSA Officer. Some states ask for a resume or professional background for the compliance officer.

Sample compliance policies — some states ask to review sample internal policies covering transaction monitoring, SAR filing, recordkeeping, and related compliance functions.

AML training program documentation — description of your AML training program including who receives training, what it covers, and how often it occurs.

Business Plan and Operational Information

A detailed business plan is required by most states. The business plan should cover your company history, ownership structure, and management team, a description of your products and services including how money flows through your platform, your target markets and customer base, projected transaction volumes by state, your technology infrastructure and payment processing relationships, your risk management approach, and your regulatory compliance strategy.

States use the business plan to understand your business model and assess whether it falls within their licensing framework. Business plans for novel fintech models typically receive more scrutiny than traditional money transmission models.

Additional State-Specific Requirements

New York requires extensive additional documentation for both its standard money transmitter license and the separate BitLicense for cryptocurrency businesses — including cybersecurity program documentation and consumer complaint handling procedures.

California requires a detailed California-specific compliance program documentation and may require an interview with DFPI staff during the application process.

Some states require a registered agent in the state — a person or entity authorized to receive legal process on behalf of your business within the state.

Some states require disclosure of your banking relationships — specifically which banks process your money transmission transactions.

Ongoing Requirements After Approval

Obtaining a money transmitter license is not the end of your compliance obligations with the state. Licensed money transmitters must meet ongoing requirements including annual license renewal, annual financial reporting covering financial condition and transaction volumes, maintenance of required net worth and surety bond, notification of material changes to business ownership, structure, or operations, and availability for periodic state examination.

Frequently Asked Questions

How far in advance should I start preparing my license application?

Given that audited financial statements take 60 to 90 days to prepare and background investigations take additional time, starting preparation at least six months before you plan to submit is prudent. For states with long processing timelines like New York and California, submitting applications 12 to 18 months before your target operational date is not unreasonable. Read more about how long applications take and how much licensing costs.

Can I submit the same application documents to multiple states through NMLS?

NMLS significantly reduces duplication by allowing you to enter company information once and use it across multiple state applications. However, state-specific documents — surety bonds, some financial statements, and state-specific disclosures — must still be tailored to each state's requirements. NMLS streamlines the process but does not eliminate all state-specific work.

What if my business does not yet have audited financial statements?

Many states provide alternative approaches for newly formed businesses — accepting reviewed or compiled financial statements combined with personal financial statements for principal owners, or requiring a capital deposit in lieu of audited financials. The specific alternatives available vary by state. Disclose your situation early in the application process and ask the state regulator what documentation they will accept.

How ComplyOne Helps

ComplyOne works with fintechs to prepare complete and well-organized money transmitter license applications, manage the application process across multiple states, and build the compliance programs that licensing strategy requires — through advisory services, compliance technology, or both.

Talk to the ComplyOne team to get started.

The information in this article is for general educational purposes and does not constitute legal or regulatory advice. Licensing requirements vary significantly by state. Verify current requirements directly with state regulators or qualified legal counsel before submitting applications.