AML compliance software automates the controls your BSA program requires. Here is what it does, what features matter, how to evaluate vendors, and what regulators expect from your compliance tech stack.

What Is AML Compliance Software? A Buyer's Guide for Fintechs

AML compliance software is a category of technology purpose-built to help financial institutions and fintechs meet their Bank Secrecy Act obligations. It automates the controls your BSA program requires — transaction monitoring, sanctions screening, KYC verification, SAR filing — so your compliance team can operate efficiently, maintain complete audit trails, and demonstrate to regulators that your program is genuinely running.

Understanding what this software does, what features actually matter for a fintech compliance program, and how to evaluate options is essential for any fintech building its compliance infrastructure.

Why AML Compliance Software Is Not Optional

At any meaningful transaction volume, BSA compliance cannot be executed manually. Consider what it takes to run a compliant AML program without automation: reviewing every transaction for suspicious patterns, screening every customer and counterparty against sanctions lists that update multiple times per week, filing SARs within 30-day deadlines while maintaining complete investigation documentation, and retaining five years of retrievable records for every compliance event. No compliance team can do this at scale without technology.

Beyond operational necessity, compliance software creates the audit trail that makes your program examinable. Timestamped, complete records of every screening event, every monitoring alert, every investigation, and every SAR filing are what you produce when regulators or sponsor banks review your program.

What AML Compliance Software Actually Does

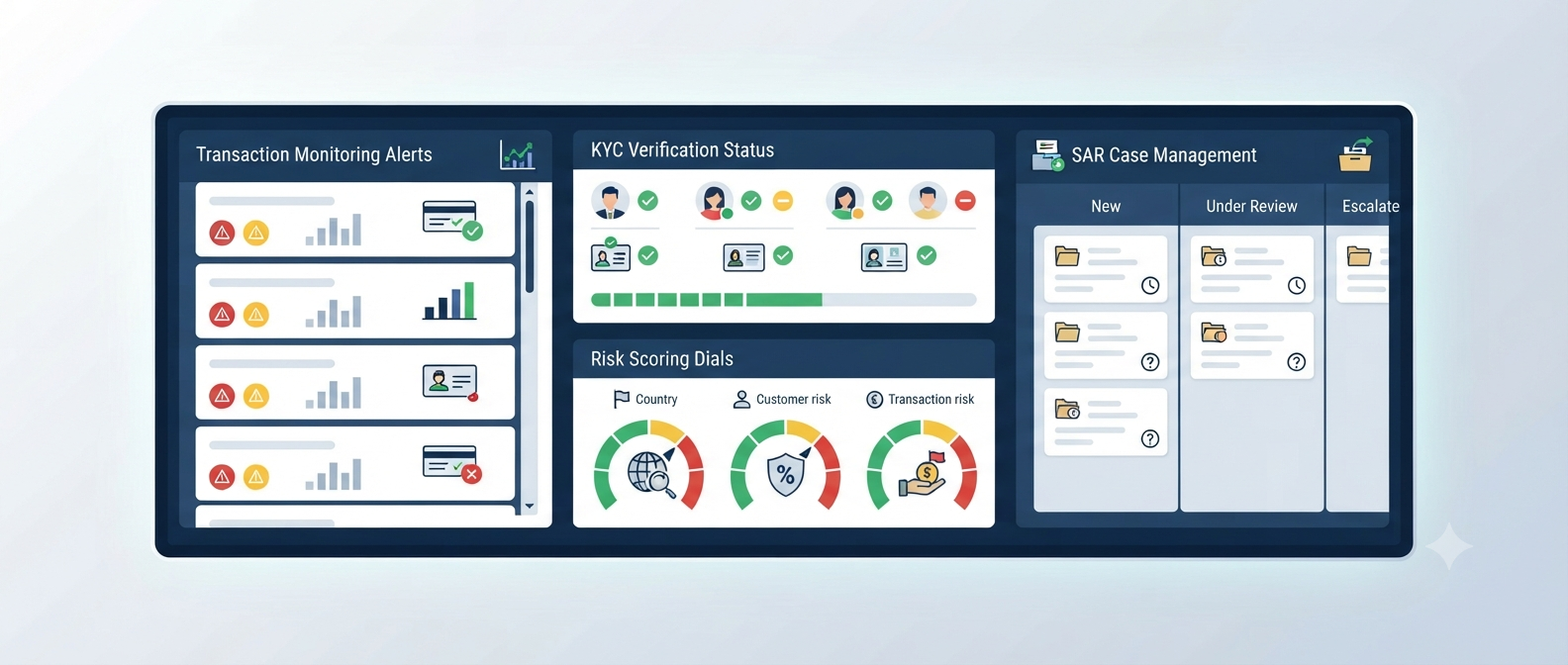

Transaction Monitoring

The core AML control function. Transaction monitoring software applies rules and behavioral models to your transaction data — continuously, across all accounts — and generates alerts when activity meets defined criteria suggesting potential financial crime. Alert management workflows route alerts to compliance analysts for review, track dispositions, and connect to SAR filing when warranted.

The most important features to evaluate are rule customizability — can you configure rules specific to your risk profile rather than relying solely on pre-built templates — and audit trail completeness — does the system produce a full timestamped record of every alert, every review decision, and every outcome.

Sanctions Screening

Automated checking of customers and transaction counterparties against OFAC's SDN List and other applicable sanctions lists, in real time at onboarding and on an ongoing basis as lists are updated. Essential features include fuzzy matching capability, automatic re-screening when lists update, and a hit review workflow with documented false positive clearing.

KYC and Identity Verification

Some AML platforms include identity verification capabilities — document verification, biometric checking, and database cross-referencing — integrated into the onboarding flow. Others integrate with dedicated KYC providers rather than providing this capability natively. Either approach can work — the key is that the onboarding verification flow is connected to the broader compliance program and produces a complete, retrievable audit trail.

Case Management and SAR Filing

When a transaction monitoring alert escalates to a suspicious activity investigation, case management functionality tracks the case from alert through resolution — attaching evidence, recording investigation steps, and producing the SAR filing when warranted. Direct integration with FinCEN's BSA E-Filing System is a significant operational convenience.

Risk Scoring and Customer Risk Rating

Many platforms produce risk scores for customers based on onboarding data — identity verification results, PEP and sanctions screening outcomes, geographic factors, and stated account purpose — feeding directly into your CDD risk rating process. Automated risk scoring improves consistency across your customer base.

Reporting and Analytics

Reporting capabilities matter for both internal oversight and external examination readiness. Look for the ability to produce alert volume and disposition reports, false positive rate trends, SAR filing statistics, and the specific record retrieval capability that regulators and sponsor banks request during reviews.

What to Look For When Evaluating Vendors

Built for Your Business Model

Some AML platforms are designed for traditional banks and their assumptions about transaction types, customer profiles, and regulatory requirements may not translate well to fintechs, MSBs, or cryptocurrency companies. Confirm that the platform's design matches your actual operation before committing.

Rule Customizability

Pre-built rule libraries are a starting point — not a finished compliance product. You must be able to configure and tune rules for your specific risk environment. A platform that does not allow meaningful rule customization will produce either excessive false positives that overwhelm your team or insufficient sensitivity that misses real suspicious activity.

Audit Trail Completeness

In a BSA examination, you must produce documentation for specific alerts, investigations, and SAR filings. Before selecting a platform, ask the vendor to show you exactly what documentation looks like for a specific alert from generation through resolution. What you see is what you will produce in an examination.

Integration Path

Your compliance software must connect to your core transaction data infrastructure. Understand the integration requirements — API availability, data format requirements, engineering work required from your team — before committing to a platform.

Pricing Scalability

Many AML platforms price by transaction volume or customer count. Model your costs at your current scale, at 5x current scale, and at 20x current scale. A platform that is affordable today may become cost-prohibitive as you grow.

Examination Support

Ask how the vendor supports customers facing regulatory examinations or sponsor bank reviews. Vendors with deep examination experience can be valuable partners when your program is reviewed — vendors who have never been through an examination with a customer may not understand what examiners actually need.

Common Mistakes When Buying AML Software

Selecting based on price alone without evaluating regulatory fitness. The cheapest option may not produce the examination-ready documentation your program needs.

Choosing a platform without adequate rule customization and then operating with generic rules that do not fit your risk profile.

Not testing the platform with realistic transaction data before go-live. Discover rule calibration issues in testing, not after your first suspicious transaction.

Treating the software purchase as the end of compliance work rather than the beginning. Technology enables your compliance program — it does not replace the human judgment, documented processes, and ongoing oversight that a compliant AML program requires.

Frequently Asked Questions

Is AML software the same as BSA compliance software?

The terms are used interchangeably in the market. BSA compliance software refers to the same category of technology — tools built to help financial institutions meet their Bank Secrecy Act obligations including transaction monitoring, sanctions screening, KYC, and SAR filing.

Do small fintechs need AML compliance software?

Yes. BSA requirements apply based on what activities you conduct — not how large you are. At even modest transaction volumes, manual compliance processes create dangerous gaps and cannot scale. Purpose-built AML software is available at price points accessible to early-stage fintechs and scales with your business.

Can I build my own AML compliance technology?

Some larger fintechs build proprietary compliance technology rather than using vendor platforms. This is a significant engineering investment that requires deep compliance expertise to do correctly. Purpose-built vendor platforms are typically the more cost-effective and faster path for fintechs who are not at significant scale and do not have large compliance engineering teams.

How ComplyOne Helps

ComplyOne offers both compliance technology and advisory expertise to help fintechs evaluate, implement, and operate AML compliance software effectively — helping you select the right tools, configure them correctly for your risk profile, and build the operational workflows that make them genuinely work.

Talk to the ComplyOne team to get started.

The information in this article is for general educational purposes and does not constitute legal or regulatory advice. Consult a qualified compliance professional for guidance specific to your situation.