Banking as a Service allows fintechs to offer financial products through sponsor banks. Here is what BaaS compliance means, what obligations fintechs take on, and how regulators are scrutinizing BaaS relationships.

What Is BaaS Compliance? Banking as a Service Requirements for Fintechs

Banking as a Service — BaaS — is the model through which fintechs access banking infrastructure, products, and regulatory coverage by partnering with FDIC-insured banks. BaaS enables fintechs to offer checking accounts, debit cards, payment processing, loans, and other financial products without obtaining their own bank charter. The bank — typically called a sponsor bank or partner bank — holds the regulatory licenses, and the fintech — often called the program manager — operates the customer-facing product.

BaaS compliance refers to the compliance obligations that arise in this structure — the obligations of both the bank and the fintech program manager — and how they are allocated, implemented, and overseen.

Why BaaS Compliance Is Different

In a traditional financial services model, the licensed institution and the customer-facing business are the same entity. BaaS splits these roles — the licensed bank and the customer-facing fintech are different companies, connected by a commercial partnership.

This creates specific compliance challenges. The bank has regulatory obligations to ensure that banking services are provided in compliance with applicable law — but the bank's customers are actually the fintech's customers, whose relationship with the bank is often indirect. The fintech has direct customer relationships and operational control over product delivery — but the regulatory obligations formally rest with the bank.

Regulators — including the OCC, FDIC, and Federal Reserve — have become increasingly focused on BaaS relationships because of the compliance risk this structure creates. Regulatory actions against sponsor banks for inadequate oversight of BaaS programs have become more common, raising the compliance stakes for both sides of the relationship.

The Fintech Program Manager's Compliance Obligations

Although the bank holds the ultimate regulatory liability, fintechs in BaaS relationships typically take on substantial compliance obligations through their program agreements and through regulatory expectation.

Core compliance obligations that fintechs typically maintain in BaaS relationships include a full BSA/AML compliance program — written policies, KYC/CDD procedures, suspicious activity monitoring, and SAR filing. The sponsor bank may also require the fintech to maintain AML controls that satisfy the bank's own compliance requirements, which may be more demanding than minimum regulatory requirements.

OFAC sanctions screening — fintechs in BaaS relationships must maintain OFAC sanctions screening for their customers and transactions. The bank retains ultimate sanctions compliance responsibility but requires the fintech to implement primary screening controls.

Consumer protection compliance — BaaS fintechs must comply with applicable consumer protection regulations including Regulation E for electronic fund transfers, UDAAP prohibitions against unfair, deceptive, or abusive practices, and other consumer financial laws. The CFPB has made clear that its consumer protection authority extends to fintech program managers in BaaS relationships.

Third-party vendor management — fintechs that use third-party technology vendors for compliance functions (identity verification, fraud detection, payment processing) must conduct appropriate vendor due diligence and oversight, as these vendors are sub-processors in the bank's vendor management framework.

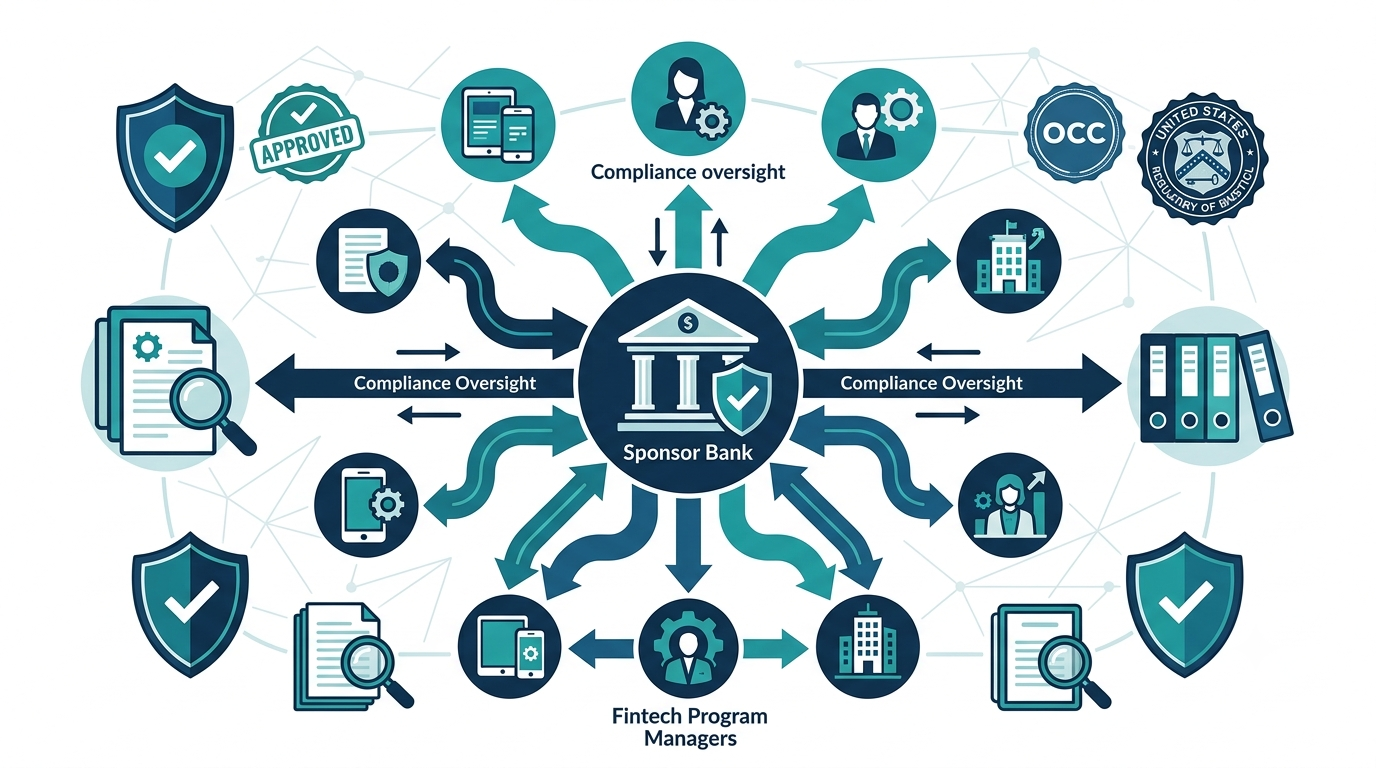

The Sponsor Bank's Oversight Obligations

Regulators expect sponsor banks to maintain meaningful oversight of their BaaS program managers — not simply to delegate compliance and trust that it is being handled. This means sponsor banks require robust compliance documentation from their fintech partners, conduct periodic audits and assessments of fintech compliance programs, require compliance metrics reporting, and may conduct transaction monitoring on the fintech's payment flows as a second layer of control.

The OCC's guidance on bank-fintech partnerships has made clear that banks cannot simply outsource their compliance obligations to fintechs and that inadequate oversight of BaaS programs creates regulatory risk for the bank. This translates into more demanding compliance requirements for fintechs seeking and maintaining sponsor bank relationships. For a full breakdown of what sponsor banks require from their fintech partners, see our guide on sponsor bank compliance.

The Regulatory Environment for BaaS Is Tightening

Regulators have issued consent orders and enforcement actions against multiple sponsor banks for inadequate oversight of their BaaS programs. These actions have created a chilling effect — many banks have exited or reduced their BaaS programs, and those that remain are imposing much more demanding compliance requirements on their fintech partners.

Fintechs seeking BaaS partnerships today face significantly more rigorous compliance due diligence from sponsor banks than was the case several years ago. Banks are conducting detailed compliance program assessments before onboarding new fintech partners and requiring ongoing compliance performance metrics as conditions of the relationship.

Frequently Asked Questions

Who is ultimately responsible for BaaS compliance — the bank or the fintech?

The bank is ultimately legally responsible for compliance with federal banking laws. However, the practical allocation of compliance responsibilities between the bank and the fintech is set by their program agreement, and fintechs that fail to meet their compliance obligations under the program agreement can face termination of the relationship — and in cases of significant violations, may face their own regulatory consequences from financial regulators and the CFPB.

What should a fintech look for in a BaaS sponsor bank?

Fintechs should look for a sponsor bank with experience in their specific product category, clear documentation of compliance expectations, realistic service level agreements for account management and compliance processes, and a track record of stable regulatory standing. Banks that have faced recent regulatory scrutiny of their BaaS programs may impose especially demanding — and potentially unstable — compliance requirements. For guidance on evaluating sponsor banks, see our guide on how to choose a sponsor bank for your fintech.

How do I know if my BaaS compliance program is sufficient?

A BaaS compliance program is sufficient when it satisfies both the requirements of your program agreement with your sponsor bank and applicable regulatory standards — and when an independent assessment confirms that it is operating effectively. Having your compliance program independently assessed before submitting it to a sponsor bank is valuable because it identifies gaps before the bank's due diligence process reveals them.

How ComplyOne Helps

ComplyOne helps fintechs build BaaS compliance programs that satisfy sponsor bank requirements, navigate the regulatory expectations around BaaS partnerships, and maintain ongoing compliance performance that keeps sponsor bank relationships stable — through advisory services, compliance technology, or both.

Talk to the ComplyOne team to get started.

The information in this article is for general educational purposes and does not constitute legal or regulatory advice. BaaS regulatory requirements are evolving. Consult qualified legal and compliance counsel for guidance specific to your BaaS partnership.