KYC — Know Your Customer — is a foundational legal requirement for most fintechs. Here is what it actually covers, what the BSA requires at onboarding and beyond, and how to build a KYC process that works.

What Is KYC? Know Your Customer Requirements for Fintechs

KYC — Know Your Customer — is one of the most widely used terms in fintech compliance, and one of the most frequently misunderstood. Many founders treat it as a synonym for identity verification. In regulatory terms, it is significantly broader than that — and getting it right is one of the most operationally important compliance decisions a fintech makes.

KYC is the end-to-end process of verifying who your customers are, understanding the nature and purpose of their relationship with your platform, assessing the risk they represent, and monitoring their activity on an ongoing basis. It is both a legal requirement under the Bank Secrecy Act and one of your most effective defenses against money laundering, fraud, and account misuse.

This article explains what KYC actually requires in regulatory terms, what the law says at each stage, and how to build a KYC process that satisfies regulators and sponsor banks while minimizing unnecessary customer friction.

What KYC Means in Regulatory Terms

In U.S. financial services regulation, KYC encompasses two distinct but closely related legal requirements.

Customer Identification Program (CIP)

The CIP is the formal, BSA-required process of collecting and verifying basic identity information from every customer at onboarding. It is the legal foundation of KYC. FinCEN requires covered financial institutions to implement a written CIP as a mandatory component of their AML program.

Your CIP must be documented in writing, applied consistently to every customer, and produce a verifiable record of the identity information collected and the verification steps taken.

Customer Due Diligence (CDD)

CDD goes significantly beyond identity verification. Added as a formal BSA requirement by FinCEN's 2016 CDD Rule, it requires covered institutions to understand the nature and purpose of each customer relationship, assign risk ratings, conduct ongoing monitoring of customer activity, and update customer information when risk profiles change.

Together, CIP and CDD constitute the complete regulatory KYC framework. CIP establishes who your customer is. CDD establishes what risk they represent and what you should expect from them.

What the CIP Requires

For individual customers, your CIP must collect and verify the following minimum information:

Full legal name — as it appears on a government-issued identity document.

Date of birth — to confirm age and support identity verification.

Residential address — a physical address, not a P.O. Box, for U.S. persons. Foreign nationals may provide their country of residence.

Identification number — for U.S. persons, a Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN). For non-U.S. persons, a passport number, alien registration number, or other government-issued document number.

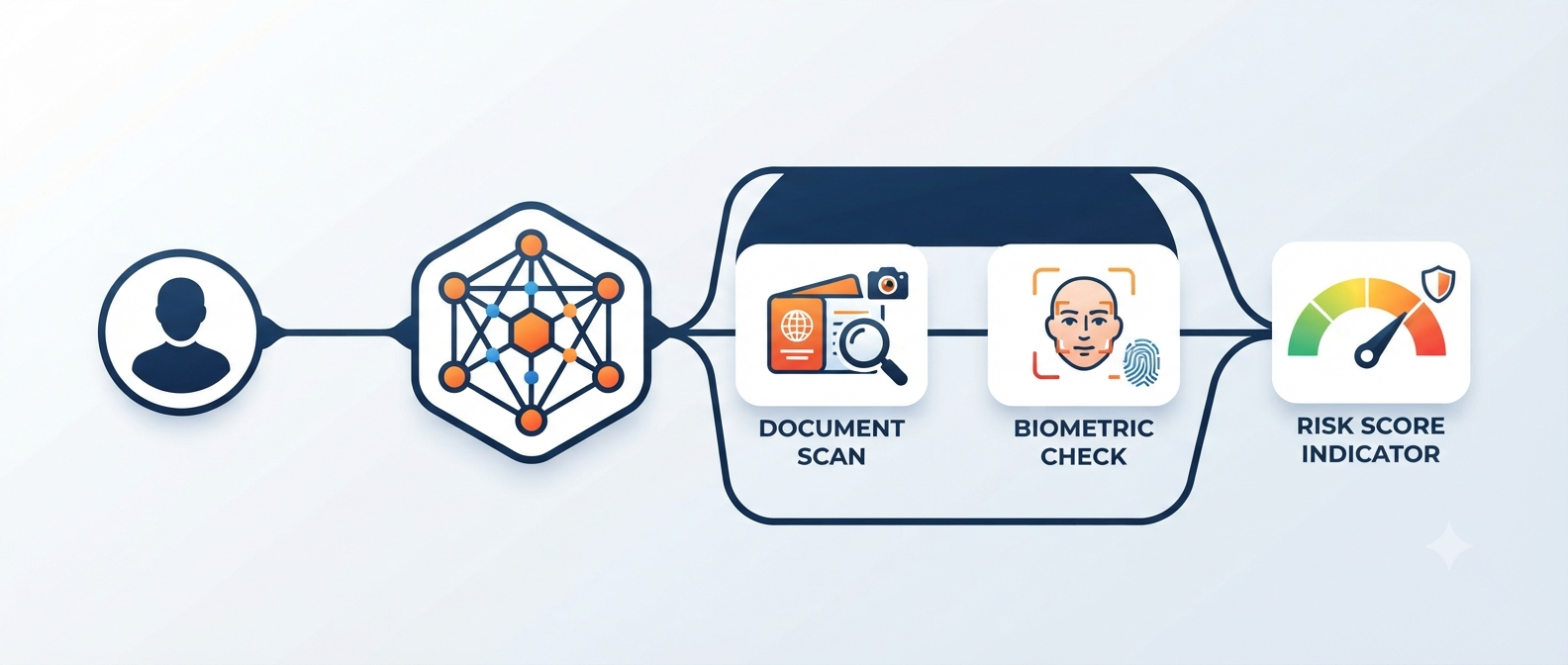

Verification means confirming the accuracy of this information — not simply collecting it. FinCEN allows two methods of verification:

Documentary verification — reviewing a government-issued identity document such as a driver's license or passport. The document must be unexpired and the information must match what the customer provided.

Non-documentary verification — cross-referencing the customer's provided information against authoritative databases such as credit bureau records, government identity databases, or third-party identity verification platforms. This is the most common method for digital-first fintechs.

Most fintechs use a combination of both methods, delivered through a third-party identity verification provider integrated into their onboarding flow.

For business customers, the CIP requires collecting and verifying:

— Legal business name and any DBA names

— Principal place of business address

— Employer Identification Number (EIN)

— Formation documents — articles of incorporation, operating agreement, or equivalent

— Beneficial ownership information for individuals who own or control the entity

What Customer Due Diligence Requires

Understand the purpose and nature of the customer relationship. At onboarding, collect information about why the customer is using your platform, what products or services they intend to use, and what type and volume of transactions you should expect from them. This expected activity profile becomes the baseline for ongoing monitoring.

Assign a customer risk rating. Based on the customer's identity, occupation or business type, source of funds, geographic location, and expected transaction behavior, assign a risk tier — typically low, medium, or high. Risk rating drives the level of monitoring and scrutiny applied to the account on an ongoing basis.

Conduct ongoing monitoring of customer activity. CDD requires continuous monitoring of customer transactions against the expected activity baseline established at onboarding. Deviations from that baseline — in volume, frequency, counterparty, or geography — trigger compliance review.

Update customer information when it changes. When a customer's circumstances change — new address, new business structure, change in transaction patterns — your CDD program must capture those changes and reassess the customer's risk profile.

Apply Enhanced Due Diligence for high-risk customers. Customers presenting elevated risk require a deeper level of scrutiny before and during the relationship — including additional documentation, source of funds verification, and more frequent periodic review.

Who Requires Enhanced Due Diligence?

Enhanced Due Diligence (EDD) applies to customers or relationships that present materially elevated money laundering or financial crime risk. Common triggers include:

— Politically Exposed Persons (PEPs) — foreign government officials, immediate family members, and known close associates

— Customers in high-risk geographies — FATF grey and black list countries, OFAC-sanctioned jurisdictions

— Customers in high-risk industries — cannabis, gambling, adult entertainment, money services, arms dealing

— Business customers with complex or opaque ownership structures — multiple layers of ownership, offshore holding companies, trust structures

— Customers with no clear or verifiable source of wealth or funds

— Customers flagged by adverse media screening for prior financial crime or regulatory violations

EDD typically involves collecting additional documentation, verifying source of funds or source of wealth, obtaining senior management approval before onboarding, and conducting more frequent periodic CDD reviews.

The Ongoing Monitoring Requirement

The ongoing monitoring requirement is where many fintech KYC programs have gaps — particularly at early stage when onboarding processes receive most of the compliance investment.

FinCEN requires that your monitoring program flags transactions that are inconsistent with the customer's established profile and triggers a CDD review when significant deviations are detected. In practice, your KYC program must be directly integrated with your transaction monitoring system so that monitoring alerts can trigger customer-level compliance reviews, not just alert-level investigations.

Periodic CDD refresh — reviewing and updating customer files at defined intervals based on risk tier — is also required. The frequency should be risk-based: at least annually for high-risk customers, every 18-24 months for medium-risk, and every 3-5 years for low-risk customers.

Building a KYC Process That Balances Compliance and Experience

KYC is your customer's first direct interaction with your compliance program. Done well, it is fast, seamless, and nearly invisible. Done poorly, it creates friction, abandonment, and reputational damage.

Key design principles:

Collect only what compliance requires. Your CIP defines the minimum. Every additional piece of information you collect during onboarding must have a specific, documented compliance reason.

Use automated technology to minimize friction. Modern identity verification platforms complete document verification and database checks in seconds with minimal customer effort. Manual review should be reserved for exceptions — not the standard flow.

Build risk-tiered onboarding. Low-risk customers in standard scenarios should move through onboarding quickly. High-risk customers triggering EDD should face additional verification steps appropriate to their risk level. Applying EDD scrutiny to every customer wastes resources and creates unnecessary friction.

Design exception workflows before they are needed. Before you launch, build the processes for customers who do not pass automated verification — non-standard ID documents, thin database files, complex business structures. These customers will exist. Having no process for them is a compliance gap.

What Regulators and Sponsor Banks Evaluate

During KYC program examinations, evaluators assess whether your CIP is written, fully implemented, and applied consistently to every customer without exception, whether required identity information is being collected and actually verified — not just collected, whether customer risk ratings are assigned consistently using defined, documented criteria, whether the ongoing monitoring program is connected to CDD — monitoring alerts trigger customer-level review where appropriate, and whether EDD is being applied to high-risk customers with appropriate documentation and oversight.

The most common examination finding in KYC reviews is inconsistency of execution — programs that require specific processes but individual customer files show those processes were not followed in specific cases. Consistency is as important as program design.

Frequently Asked Questions

What is the difference between KYC and AML compliance?

KYC (Know Your Customer) is a specific component of a broader AML compliance program. AML compliance encompasses the full set of Bank Secrecy Act obligations — including AML policies, transaction monitoring, SAR filing, training, and independent testing. KYC — specifically the CIP and CDD requirements — is the customer-facing element of an AML program that establishes who customers are and what risk they represent.

When must KYC be completed — before or after account opening?

Under FinCEN's CIP rules, covered institutions must collect required identity information before or at the time of account opening, and must verify that information within a reasonable time. For most digital fintech products, verification should be completed before the customer is permitted to conduct any transactions. Allowing customers to transact before verification is complete is a significant compliance and fraud risk.

Does KYC apply to all customers or just high-risk ones?

KYC applies to all customers without exception. The CIP requirement to collect and verify identity information is universal — it does not have a risk threshold. What varies based on risk rating is the depth of CDD conducted, the level of ongoing monitoring applied, and whether Enhanced Due Diligence is required. But every customer must go through your basic CIP process.

How long must KYC records be retained?

BSA regulations require that customer identification records — including the information collected and the verification steps taken — be retained for five years after the account is closed. CDD records including risk ratings, ongoing monitoring documentation, and periodic review records must also be retained for the BSA-required minimum period.

How ComplyOne Helps

ComplyOne helps fintechs design CIP and CDD programs that meet FinCEN requirements, select and implement identity verification technology, build risk-tiered onboarding flows, and establish the ongoing monitoring workflows that keep KYC programs current and examination-ready — through compliance technology, advisory services, or both.

Talk to the ComplyOne team to get started.

The information in this article is for general educational purposes and does not constitute legal or regulatory advice. Compliance requirements vary based on your business model, jurisdiction, and regulatory relationships. Consult a qualified compliance professional for guidance specific to your situation.